Page 1

Entrepreneurial activity at the present stage increasingly depends on economic information. The quality of such information determines the profitability of decisions made, including determining the circle of clients, suppliers and possible partners. At the same time, increasing importance is being attached to the completeness and reliability of information about financial results and the conditions under which they occurred. The most common source of such information is accounting (financial) statements.

The basic rules on accounting statements are determined by the Federal Law “On Accounting” No. 129-FZ dated November 21, 1996 and the Regulations on Accounting and Financial Reporting in the Russian Federation dated No. 34n on July 29, 1998. These norms were developed in the Regulations on accounting “Accounting statements of an organization” (PBU 4/99) No. 43n dated 07/06/99

The practical content of the concepts of accounting reporting on financial results is regulated by a number of documents of the third level of regulatory regulation of accounting. The main ones include “Instructions on the scope of financial reporting forms” (hereinafter referred to as Instructions) No. 4n dated January 13, 2000. The procedure for the formation of financial performance indicators in the financial statements in relation to the established forms is mainly determined by the “Methodological recommendations on the procedure for the formation of financial reporting indicators organization" (hereinafter - Methodological Recommendations) No. 60n dated June 28, 2000. You should immediately pay attention to the target orientation of the specified document - recommendations, i.e. the procedure for forming individual indicators is of a recommendatory nature.

In accordance with the instructions, indicators of financial results and use of profits are presented in the “Balance Sheet” (Form No. 1), in the “Profit and Loss Statement” (Form No. 2) and in the “Statement of Changes in Capital” (Form No. 3 ).

The most significant reporting form on the financial results of the reporting period is the Profit and Loss Statement, which presents data defined by the accounting regulations in force on the date of its preparation as indicators of financial results.

The procedure for generating the Profit and Loss Statement is regulated by Section 3 “The procedure for generating data on the Profit and Loss Statement (Form No. 2)” of the above Methodological Recommendations. In turn, the development of methodological recommendations was carried out on the basis of basic standards in PBU 9/99 “Income of the organization” and PBU 10/99 “Expenses of the organization”.

The first section, “Income and expenses from ordinary activities” (p. 010), presents the most important estimated indicators of the organization’s economic activities. Income from ordinary activities includes revenue recognized by the organization, which is reflected in the report item “Revenue (net) from the sale of goods, products, works, services (less value added tax, excise taxes and similar mandatory payments).” In turn, expenses include cost of sales, as well as selling and administrative expenses. In this case, the indicators are formed according to the moment at which the accounting object is considered sold, the decision on which is fixed in the accounting policy of the organization.

Cost of sales includes all direct expenses that are recognized in the sale of goods and services for which revenue is determined and are directly used to generate revenue from the sale. This indicator is reflected in the article “Cost of goods, products, works, services sold” (line 020). The value of this indicator directly depends on the elements of accounting policy chosen by the organization and, accordingly, also affects the value of the financial result.

Selling expenses (selling expenses) represent the costs of marketing, advertising, salaries of sales staff, delivery of products to the consumer, as well as overhead costs incurred in the course of sales activities. This indicator is reflected in the report item “Business expenses” (line 030). The amount of these expenses also depends on the elements of the accounting policy chosen by the organization.

In the income statement, the Organization's income for the reporting period is reflected as a division into revenue and other income.

The Explanations to the Balance Sheet and the Profit and Loss Statement disclose information about the types of revenue and other income that constitute five percent or more of the total revenue and other income, respectively.

In the balance sheet, the balance of account 46 “Completed stages of work in progress” is reflected in the item “Accrued revenue not presented for payment” of the group of items “Inventories”.

The following other income and expenses are shown on a net basis in the income statement:

1) income and expenses in the form of exchange rate differences;

2) income and expenses from transactions of purchase and sale of foreign currency;

3) contributions to valuation reserves and income in the form of amounts of restored valuation reserves;

4) expenses for reserves for contingent facts of economic activity and income in the form of amounts of restored reserves for contingent facts of economic activity;

5) income and expenses from the revaluation of securities at market value;

6) income and expenses from the disposal of fixed assets, objects of unfinished construction, with the exception of disposal as a result of the purchase and sale of these objects.

10. Cost accounting

Expenses of the Organization are recognized as a decrease in economic benefits as a result of the disposal of assets (cash, other property) and (or) the occurrence of liabilities, leading to a decrease in the capital of the Organization, with the exception of a decrease in contributions by decision of participants (owners of property).

The expenses of the Organization, depending on their nature, conditions of implementation and areas of activity of the Organization, are divided into:

1) expenses for ordinary activities;

2) other expenses.

Expenses for ordinary activities - expenses associated with the manufacture of products and the sale of products, the acquisition and sale of goods. Such expenses also include expenses the implementation of which is associated with the performance of work or provision of services.

Expenses for ordinary activities of the Organization are expenses the implementation of which is associated with ordinary activities.

Expenses other than expenses for ordinary activities are considered other expenses.

Other expenses of the Organization are:

expenses associated with the provision for a fee for temporary use (temporary possession and use) of the Organization’s assets (provided that they are different from expenses for ordinary activities);

expenses associated with the provision for a fee of rights arising from patents for inventions, industrial designs and other types of intellectual property (provided that they are different from expenses for ordinary activities);

expenses associated with participation in the authorized capital of other organizations (provided that they are different from expenses for ordinary activities);

expenses associated with the sale, disposal and other write-off of fixed assets and other assets other than cash (except foreign currency), goods, products;

interest paid by the Organization for the provision of funds (credits, loans) to it for use;

expenses related to payment for services provided by credit institutions;

contributions to valuation reserves created in accordance with accounting rules (reserves for doubtful debts, for depreciation of investments in securities, etc.), as well as reserves created in connection with the recognition of contingent facts of economic activity;

fines, penalties, penalties for violation of contract terms;

compensation for losses caused by the Organization;

losses of previous years recognized in the reporting year;

amounts of receivables for which the statute of limitations has expired, and other debts that are unrealistic for collection;

exchange differences;

the amount of asset depreciation;

the amount of variation margin to be paid;

transfer of funds (contributions, payments, etc.) related to charitable activities, expenses for sporting events, recreation, entertainment, cultural and educational events and other similar events;

other expenses.

Other expenses are also expenses that arise as a consequence of emergency circumstances of economic activity (natural disaster, fire, accident, nationalization of property, etc.).

In accordance with PBU 9/99, at least the following information is subject to disclosure as part of information about the organization’s accounting policies in the financial statements:

* on the procedure for recognizing the organization’s revenue;

* on the method of determining the readiness of works, services, products; Revenue from completion and sale of which is recognized when ready.

Revenue, operating and non-operating income, amounting to 5% and more of the total income for the reporting period are shown for each type of activity. Accordingly, income for each type of activity must be reflected in the reporting and expenses by type of activity (requirements of PBU 10/99).

For revenue received as a result of the execution of contracts providing for the fulfillment of obligations in non-monetary means, the following information must be disclosed:

* the total number of organizations with which these agreements were concluded, indicating the organizations that account for the bulk of such revenue;

* share of revenue received under these agreements with related organizations;

* method of determining the cost of products (goods) transferred by the organization.

Other income of the organization for the reporting period that is not credited to the profit and loss account is subject to disclosure in the financial statements separately.

The construction of accounting should ensure the possibility of disclosing information about the organization’s income in the context of current, investment and financial activities.

The main components of the organization's financial result are shown in the income statement. Operating and non-operating income may be reported in the income statement less expenses related to these income when:

* the relevant accounting rules provide for or do not prohibit such recognition of income;

* income and related expenses arising as a result of the same or similar fact of economic activity are not significant for characterizing the financial position of the organization. Kondrakov N.P. Accounting: Textbook. - INFRA-M, 2006 - pp. 397-398

CONCLUSION

As discussed in this work, in a market economy, the importance of profit is enormous. The desire to make a profit directs commodity producers to increase the volume of production of products needed by the consumer and reduce production costs. With developed competition, this achieves not only the goal of entrepreneurship, but also the satisfaction of social needs. For an entrepreneur, profit is a signal indicating where the greatest increase in value can be achieved, creating an incentive to invest in these areas. Losses also play a role. They highlight mistakes and miscalculations in the direction of funds, organization of production and sales of products.

To improve the efficiency of an enterprise, it is of paramount importance to identify reserves for increasing production and sales volumes, reducing the cost of products (works, services), and increasing profits. The factors necessary to determine the main directions for searching for reserves for increasing profits include natural conditions, government regulation of prices, tariffs, etc. (external factors); change in the volume of means and objects of labor, financial resources (internal production extensive factors); increasing the productivity of equipment and its quality, accelerating the turnover of working capital, etc. (intensive); supply and sales activities, environmental protection activities, etc. (non-production factors).

The work analyzes: the composition and structure of balance sheet profit, analysis of factors in the formation of the enterprise's balance sheet profit and analysis of the assessment of its dynamics; factor analysis of profit from sales of products (works, services) and other sales; analysis of profits (losses) from non-operating operations, analysis of factors in the formation of profit from financial and economic activities, analysis of the composition and structure of taxable profit.

The accounting theory of our country and established accounting practice reflect the opinion of the majority of domestic experts that in the Russian Federation the main form of accounting reporting is the balance sheet. In Russian conditions this is quite understandable. Complex economic realities, the impossibility of the loan capital market, the crisis of non-payments, lead to the fact that information about capital structure and financial stability comes to the fore, and not about economic attractiveness for investors and lenders. In a country with a stable economy, information about the process of generating financial results in a variety of areas of activity is of utmost importance. And what comes to the fore is not hiding profits, but proving one’s competitiveness and the ability to quickly increase one’s own and other people’s capital.

Business entities aimed at making a profit today are highly dependent on economic information. The quality of this information influences profitability through decisions made, including the identification of customers, suppliers and potential partners. The source of this information may be financial statements.

Note 1

Accounting and other financial statements must contain reliable data and give a complete picture of the financial condition of the enterprise as of a certain date and the financial results of its activities, which is necessary for users of these statements to make the right economic decisions.

Contents of financial statements

The content of financial statements, including data on financial results, is regulated by accounting regulatory documents. The algorithm for calculating financial performance indicators in reporting is determined by the “Methodological Recommendations on the Procedure for Forming Indicators of an Organization’s Accounting Reports.” The provisions of this document are advisory in nature. The main indicators of the use of profit and financial results are indicated in the Balance Sheet, in the Statement of Financial Results and in the Statement of Changes in Capital.

The greatest importance belongs to the reporting form on financial results - the Statement of Financial Results. It reflects the data defined by regulatory documents as an indicator of financial results.

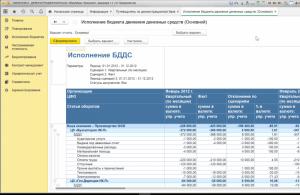

Figure 1. Disclosure of information about income in financial statements

Figure 1 shows the main section of the Income Statement.

Income statement

The rules for generating the Statement of Financial Results are established by the third section of the Methodological Recommendations, entitled “Procedure for generating income statement data.”

The first section of the report contains information about the estimated performance indicators of the enterprise. Income from ordinary activities includes revenue recognized by the company and reflected in the report in the line “Revenue” without value added tax. Expenses include the cost of these sales, commercial and administrative expenses.

The cost of sales takes into account direct expenses in full, recognized when selling goods and services, with a certain amount of revenue, and aimed at generating income from sales. This indicator is indicated in the article “Cost of sales” in line 2120 of the report. The value of this indicator is directly dependent on the accounting policy of the enterprise and directly affects the financial result.

Selling expenses, or, as they are also called, selling expenses, include expenses for advertising, marketing activities, wages of sales department employees, delivery of products to the consumer and other overhead costs that arise during the sales process. The indicated indicator is indicated in the report article “Business expenses”, in line 2210.

In the report article “Administrative expenses”, line 2220 indicates expenses associated with managing the enterprise, as well as general expenses that are not associated with the production of specific types of products or services. Such expenses are reflected in the report provided that the company calculates the cost of sales using the direct-costing principle, i.e. reduced cost. The procedure for calculating cost and reflecting overhead costs must be fixed in the accounting policy of the enterprise.

Interim results that characterize the ordinary activities of the enterprise qualitatively and are presented as gross profit and profit or loss from sales are highlighted in the first section of the “Report on Financial Results” for the articles of the same name.

Line 2100 under the item “Gross profit” indicates the difference between income from ordinary activities and direct expenses. This indicator is calculated based on data from the “Income Statement” and is not reflected in the accounting registers. Its main function is informational for economic analysis and determining the profitability of manufactured products, determining the break-even of production.

Line 2200 in the item “Profit or loss from sales” indicates the difference between income from ordinary activities and all types of expenses. This indicator is one of the most important in the system of evaluation indicators of the entire activity of the organization and characterizes the direction of activity for which this organization was created.

The articles “Other income” and “Other expenses” present indicators of income and expenses for those operations that are both recurring and normal for the enterprise, but are not part of normal activities. The indicators of interest receivable and interest payable are separately highlighted in lines 2320, 2330; these are income and expenses from the payment and receipt of interest payments. This section also reflects income from participation in other organizations on line 2310; in fact, this is the receipt of dividends on the invested capital of the enterprise.

After filling out the data for the items discussed above in the “Income Statement”, a subtotal is calculated showing the presence of profit or loss before tax. This total is calculated directly from the report data and is not reflected in system accounting. Here, in line 2410, tax payments are reflected.

The result of the “Income Statement” is the final financial result of the enterprise and is presented as net profit or loss of the reporting period in line 2400 of the report.

The value of this indicator is quite large. This is an important aggregate indicator characterizing the activities of the enterprise for the reporting year. At the same time, this is the amount that reflects the growth or decline in the well-being of the owners of this enterprise. This indicator is inextricably linked with the development of the company’s activities in subsequent periods.

The basic economic principles for reporting financial results are as follows:

- avoidance of offsets between items of income and expenses, reflection of all expenses and income in full;

- breakdown of income and expenses by type;

- reflection of income and expenses arising in the reporting period depending on the relationship of their causes to the reporting period.

Note 2

It should be noted that other expenses may not be indicated in the Financial Results Statement in detail in relation to the corresponding income, if the expenses, as well as the income associated with them, arose as a result of the same fact of economic activity and are not significant for characterizing the financial position of the enterprise .

- 218.00 KbFEDERAL AGENCY FOR EDUCATION

STATE EDUCATIONAL INSTITUTION

HIGHER PROFESSIONAL EDUCATION

"SAINT PETERSBURG STATE UNIVERSITY

ECONOMICS AND FINANCE"

Faculty of Statistics, Accounting and Economic Analysis

Department of Accounting and Auditing

Allow for protection

Scientific director

/_____________________/

"____"__________ 2009

COURSE WORK

in the course "Accounting Theory"

Students of group 458

Belenova Alina Alexandrovna

on the topic of: GENERATION OF INFORMATION ABOUT INCOME AND EXPENSES OF THE ORGANIZATION

Scientific adviser:

Saint Petersburg

2009

ABOUT THE CHAPTER

INTRODUCTION

New business conditions and accounting reform in the Russian Federation have led to significant changes in the methodology and organization of accounting. The powers of organizations to reflect their own business transactions have expanded significantly. They independently choose methods for assessing inventories and methods for calculating the cost of work, develop accounting policies, and determine specific methods, forms and techniques for maintaining and organizing accounting. In other words, at present, only general accounting rules are centrally established, and their specification and implementation mechanism are developed in each organization independently, based on the conditions of its activities.

The relevance of the chosen research topic is determined by the fact that maintaining the required level of profitability is an objective law of the normal functioning of an organization in a market economy. The systematic lack of profit and its unsatisfactory dynamics indicate the inefficiency and riskiness of the business.

Thus, the final object of accounting is the financial results of the organization’s activities and factors affecting the quality (profit or loss) and size of financial results, namely, the organization’s income and expenses.

The purpose of writing this work is to study the formation of accounting information about the income and expenses of an organization. To achieve this goal it is necessary:

- reveal the essence and meaning of accounting for income and expenses;

- study the classification of income and expenses;

- analyze the composition of income and expenses from ordinary activities, as well as other income and expenses;

- analyze the methodological foundations and rules for accounting for income and expenses;

- consider ways to estimate income and expenses;

- consider the procedure for generating financial results.

- Compare income and expenses in Russian accounting and in IFRS.

This course work consists of two chapters, a list of references consisting of 17 sources and a conclusion.

The first chapter examines the essence and significance of income and expenses, as well as the conditions for acceptance for accounting. The second chapter defines the accounting of income and expenses of an organization, the objectivity of the assessment of income and expenses, the rules for accounting for income and expenses, and a comparison of the accounting of income and expenses with IFRS and Russian accounting.

The theoretical and methodological basis of this work was the works of modern domestic economists engaged in research on the topic of accounting for income and expenses of an organization, current regulatory legal acts, educational and methodological manuals on accounting, periodical articles and others. A complete list of sources used is given at the end of the work.

In conclusion, the main conclusions and proposals obtained during the study are formulated.

1. ESSENCE OF INCOME AND EXPENSES IN MODERN ECONOMIC CONDITIONS

1.1. The concept of income and expenses of an organization

Since 2000, organizations have formed accounting information on income and expenses in accordance with the procedure established by the Ministry of Finance of Russia in the Accounting Regulations “Income of the Organization” (hereinafter referred to as PBU 9/99) and “Expenses of the Organization” (hereinafter referred to as PBU 10/99) , approved by Orders No. 32n and No. 33 dated 05/06/1999. These Regulations establish the methodological basis for the formation and reflection in accounting of reliable information about the income received from the entrepreneurial activities of the organization. This makes it possible to solve such problems as operational management and control over the activities of the organization by persons who have a direct or indirect interest in its affairs. The concept of income and expenses underlying the mentioned PBUs is that not all costs are expenses, just as not all receipts are income.

In accounting, according to clause 2 of PBU 9/99, an organization’s income is recognized as an increase in economic benefits as a result of the receipt of assets (cash, other property) and (or) repayment of liabilities, leading to an increase in the capital of this organization, with the exception of contributions of participants (owners) property). 1

In other words, funds or other property received over a certain period form the organization’s income, increasing its assets. Receipts from other legal entities and individuals are not recognized as income of the organization, for example:

- amounts of value added tax, excise taxes, sales tax, export duties and other similar mandatory payments

- under commission agreements, agency and other similar agreements in favor of the principal, principal, etc.;

- in advance payment for products, goods, works, services;

- advances in payment for products, goods, works, services;

- deposit;

- as collateral, if the agreement provides for the transfer of the pledged property to the pledgee;

- in repayment of a loan granted to the borrower.

All these receipts, although they replenish the current account (or cash desk) of the organization, are not its income, because belong to other legal entities (or budgets of different levels) and do not contribute to increasing its capital. However, not every increase in capital is a consequence of income growth. For example, if the owner invests additional funds, the organization’s capital increases, but these proceeds are not included in its income (by definition). 2

Since income is recognized under certain conditions, clause 12 of PBU 9/99 contains five such conditions:

1) the organization has the right to receive revenue arising from a specific agreement or confirmed in another appropriate manner;

2) the amount of revenue can be determined;

3) there is confidence that as a result of a specific transaction there will be an increase in the economic benefits of the organization or there is no uncertainty in their receipt;

4) the right of ownership (possession, use and disposal) of the product (goods) has passed from the organization to the buyer or the work has been accepted by the customer, the service has been provided;

5) the expenses that have been incurred or will be incurred in connection with this operation can be determined.

Without the mandatory fulfillment of these conditions, income is not recognized in a specific reporting period, but is reflected in accounting either as receivables (when cash or other property is not received) or as accounts payable (when cash or other property is received).

To recognize in accounting revenue from the sale of products and goods, performance of work and provision of services, i.e. When it is clear that a condition for the transfer of title must be fulfilled, all five conditions listed must be satisfied.

To recognize income, the receipt of which is not associated with the transfer of ownership and (or) in the absence of expenses associated with its receipt, three or four recognition conditions must be met, respectively. 3

Speaking about income recognition, it should also be noted that along with the short cycle of creating finished products, performing work and providing services (up to 12 months), there are also products (work, services) for which the normal operating cycle exceeds 12 months, for example , when determining income in construction or when conducting R&D. The rules for recognizing such income are given in paragraph 13 of PBU 9/99. An organization may reflect in its accounting revenues from the sale of products (performance of work, provision of services) with a long production cycle either upon completion of its production, or gradually as it is ready, if on the basis of primary accounting documents it is possible to determine the amount (or percentage) of the readiness of the product (work , services).

If the amount of proceeds from the sale of products (performance of work, provision of services) cannot be determined (for example, there are no world analogues of the manufactured products), the proceeds are accepted for accounting in the amount of expenses recognized in accounting for the manufacture of these products, the performance of this work, the provision of this services. Moreover, for products that are different in nature and conditions for manufacturing, performing work and providing services, an organization can use different methods of revenue recognition in one reporting period. Information about the chosen method should be reflected in the accounting policies of the organization.

Other income is recognized in accounting in the following order 4:

Proceeds from the sale of fixed assets and other assets other than cash (except foreign currency), products, goods, as well as interest received for the provision of funds to the organization for use, and income from participation in the authorized capital of other organizations (when this is not subject of the organization's activities).In this case, for accounting purposes, interest is accrued for each expired reporting period in accordance with the terms of the agreement;

Fines, penalties, penalties for violation of contract terms, as well as compensation for losses caused to the organization - in the reporting period in which the court made a decision to collect them (or the buyer (customer) was recognized as a debtor);

Amounts of accounts payable and depositors for which the statute of limitations has expired - in the reporting period in which the statute of limitations expired;

Amounts of revaluation of assets - in the reporting period to which the date as of which the revaluation was made;

- other receipts - as they are formed (identified).

The accounting regulation “Expenses of an organization” (PBU 10/99) establishes the rules for the formation in accounting of information on the expenses of commercial organizations (except for credit and insurance organizations) that are legal entities under the legislation of the Russian Federation.

In turn, in accordance with clause 2 of PBU 10/99, an organization’s expenses are recognized as a decrease in economic benefits as a result of the disposal of assets (cash, other property) and (or) the occurrence of liabilities, leading to a decrease in the capital of this organization, with the exception of a decrease in deposits by decision of the participants (property owners).

However, the main thing in understanding the definition of “expenses” should be the purpose that this category is intended to achieve. This goal should be considered to be the achievement of the ability to calculate the financial result of an organization as the difference between its income and expenses for a certain period. Based on this, PBU 10/99 contains a number of restrictions on types of expenses, which, being essentially 100% expenses, are not recognized as such in relation to its purposes, since they do not directly affect the formation of financial results 5 . Content

INTRODUCTION 3

1. ESSENCE OF INCOME AND EXPENSES IN MODERN ECONOMIC CONDITIONS 5

1.1. The concept of income and expenses of an organization 5

1.2. Classification and characteristics of income and expenses 11

2. PRINCIPLES OF ACCOUNTING INCOME AND EXPENSES 15

2.1. Methodological principles and rules for accounting for income and expenses 15

2.2. Methods for assessing income and expenses 18

2.3. Comparison of income and expenses in Russian accounting and IFRS 24

CONCLUSION 27

LIST OF REFERENCES AND ELECTRONIC SOURCES 29

APPENDIX 31